Navigating 2026 Student Loan Landscape: Repayment & Forgiveness Updates

The landscape of student loans is in constant flux, and as we approach 2026, it’s more crucial than ever for borrowers to understand the changes, opportunities, and challenges that lie ahead. The decisions made today regarding your student loan repayment can significantly impact your financial future. This comprehensive guide aims to shed light on the evolving environment, focusing on key repayment options, potential forgiveness programs, and essential updates that will shape the student loan 2026 experience.

For millions of Americans, student debt is a significant financial burden. The sheer volume of outstanding student loans necessitates a proactive approach to management and a deep understanding of available resources. Whether you are a recent graduate, a seasoned professional still paying off loans, or a prospective student considering future borrowing, staying informed about the student loan 2026 outlook is paramount. We will delve into the intricacies of federal and private loans, explore various repayment strategies, and highlight the latest developments in loan forgiveness initiatives.

Understanding the Current Student Loan Environment

Before we project into 2026, it’s important to grasp the current state of student loans. The past few years have seen unprecedented changes, from payment pauses and interest waivers during the pandemic to significant policy shifts and new repayment plans. These changes have reset expectations for many borrowers and underscored the need for continuous vigilance regarding their loan status.

Federal vs. Private Student Loans: What’s the Difference?

A fundamental distinction lies between federal and private student loans. Federal student loans are issued by the U.S. Department of Education and come with a range of borrower protections and benefits, including flexible repayment options, deferment, forbearance, and access to forgiveness programs. Private student loans, on the other hand, are offered by banks, credit unions, and other private lenders. They typically have fewer borrower protections and their terms are often less flexible, making federal loans the preferred option for most students.

The student loan 2026 environment will likely continue to emphasize these differences. Federal programs are subject to legislative changes and administrative adjustments, which can create both challenges and opportunities. Private loans, while sometimes offering competitive interest rates for highly qualified borrowers, generally remain outside the scope of most government-led relief efforts.

Key Repayment Options for 2026 and Beyond

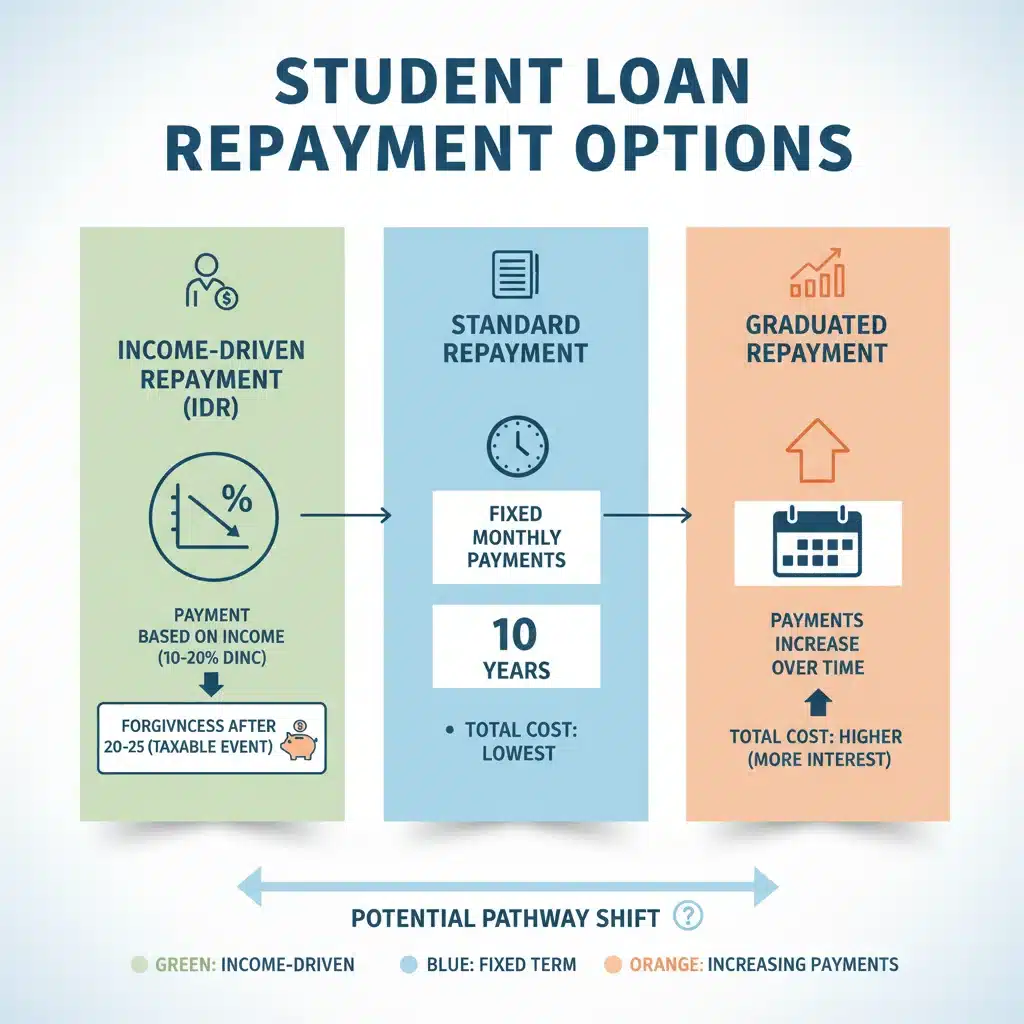

Navigating the various repayment plans can be daunting. As we look towards 2026, understanding your options is crucial for effective debt management. Federal student loans offer several repayment plans designed to accommodate different financial situations. Here are the primary categories:

1. Standard Repayment Plan

This is the default plan for most federal student loans. Under the Standard Repayment Plan, you pay a fixed amount each month until your loans are paid in full, typically over 10 years. While it results in the lowest total interest paid over the life of the loan, the monthly payments can be higher than other plans, especially for those with significant debt.

2. Graduated Repayment Plan

The Graduated Repayment Plan starts with lower payments that gradually increase every two years. This plan is also typically for a 10-year term. It can be beneficial for borrowers who expect their income to increase over time, allowing them to manage lower initial payments while still aiming for a relatively quick repayment.

3. Extended Repayment Plan

For borrowers with more than $30,000 in federal student loan debt, the Extended Repayment Plan offers lower monthly payments over a period of up to 25 years. Payments can be fixed or graduated. While this plan significantly reduces monthly costs, it means paying more interest over the long term.

4. Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are perhaps the most critical options for borrowers struggling with high monthly payments relative to their income. These plans adjust your monthly payment amount based on your income and family size, typically capping payments at a percentage of your discretionary income. Any remaining balance after a certain number of years (usually 20 or 25, depending on the plan) is forgiven, though the forgiven amount may be subject to income tax.

There are several types of IDR plans, and understanding the nuances of each will be vital for the student loan 2026 landscape:

- REPAYE (Revised Pay As You Earn): Generally caps payments at 10% of discretionary income.

- PAYE (Pay As You Earn): Also caps payments at 10% of discretionary income, but often has different eligibility requirements than REPAYE.

- IBR (Income-Based Repayment): Caps payments at 10% or 15% of discretionary income, depending on when you took out your loans.

- ICR (Income-Contingent Repayment): The oldest IDR plan, capping payments at 20% of discretionary income or what you’d pay on a fixed 12-year plan, whichever is less.

- SAVE Plan (Saving on a Valuable Education): This is the newest IDR plan, replacing REPAYE. The SAVE Plan offers significant benefits, including a lower discretionary income calculation for undergraduate loans (5% instead of 10% for some loans starting July 2024), and an interest subsidy that prevents your balance from growing as long as you make your monthly payment, even if the payment is $0. This plan is expected to be a cornerstone of the student loan 2026 environment.

Choosing the right IDR plan requires careful consideration of your income, family size, loan types, and future financial projections. It’s highly recommended to use the Loan Simulator tool on StudentAid.gov to compare plans and determine the best fit for your situation as you prepare for student loan 2026.

Student Loan Forgiveness Programs and Updates for 2026

Beyond standard repayment, several programs offer the possibility of having a portion or all of your federal student loans forgiven. These programs often have strict eligibility requirements and specific service commitments. As we approach student loan 2026, it’s vital to stay updated on these initiatives.

1. Public Service Loan Forgiveness (PSLF)

PSLF is designed for borrowers who work full-time for a U.S. federal, state, local, or tribal government or a non-profit organization. After making 120 qualifying monthly payments under a qualifying repayment plan (typically an IDR plan), the remaining balance on your Direct Loans is forgiven. The payments do not have to be consecutive. PSLF has seen significant improvements in recent years, including temporary waivers that allowed more payments to count towards forgiveness. It’s crucial for public servants to ensure they meet all criteria and submit their Employment Certification Form (ECF) regularly.

2. Teacher Loan Forgiveness (TLF)

Teachers who work full-time for five consecutive, complete academic years in certain low-income schools or educational service agencies may be eligible for forgiveness of up to $17,500 on their Direct Subsidized and Unsubsidized Loans and their Subsidized and Unsubsidized Federal Stafford Loans. The specific amount depends on the subject taught. This program will continue to be an important relief option for qualifying educators in the student loan 2026 period.

3. Total and Permanent Disability (TPD) Discharge

Borrowers who are totally and permanently disabled may be eligible to have their federal student loans discharged. This can be demonstrated through a Department of Veterans Affairs (VA) disability determination, a Social Security Administration (SSA) disability notice, or a physician’s certification. The TPD discharge provides significant relief but often comes with a three-year monitoring period to ensure the borrower’s income doesn’t exceed certain thresholds.

4. Borrower Defense to Repayment

This program offers relief to students whose schools engaged in misconduct, such as misrepresenting job placement rates or program quality. If approved, the borrower’s federal student loans may be discharged. Recent administrations have streamlined this process and approved significant amounts of relief. Borrowers who believe they were defrauded by their institutions should explore this option for student loan 2026.

5. Closed School Discharge

If your school closed while you were enrolled or shortly after you withdrew, you might be eligible for a closed school discharge, provided you did not complete your program or transfer your credits to a similar program. This can cancel 100% of your federal student loans obtained to attend that school.

6. The SAVE Plan’s Path to Forgiveness

As mentioned earlier, the SAVE Plan includes a forgiveness component. For borrowers with original principal balances of $12,000 or less, the remaining loan balance can be forgiven after as few as 10 years of payments. This is a significant improvement over other IDR plans, which typically require 20 or 25 years. This accelerated path to forgiveness will be a game-changer for many low-balance borrowers in the student loan 2026 environment.

Preparing for Student Loan 2026: Actionable Steps

Proactive planning is key to navigating your student loans effectively. Here are essential steps to take as you look towards 2026:

1. Understand Your Loan Details

Log in to StudentAid.gov to access your federal student loan history, including loan types, interest rates, and current servicer. For private loans, check with your lender. Knowing these details is the first step in making informed decisions about your student loan 2026 strategy.

2. Evaluate Your Repayment Options

Use the Loan Simulator tool on StudentAid.gov. This tool allows you to compare different repayment plans, including IDR options, and see how they impact your monthly payment, total interest paid, and potential forgiveness. This is especially important given the new SAVE Plan.

3. Consider Consolidating Your Federal Loans

Federal Direct Loan Consolidation can simplify your repayment by combining multiple federal loans into a single loan with one monthly payment. It can also make you eligible for certain IDR plans and PSLF if you have older federal loans (like FFEL Program loans) that wouldn’t otherwise qualify. Be aware that consolidation might reset your payment count for forgiveness programs, so weigh the pros and cons carefully.

4. Explore Refinancing Private Loans

If you have private student loans, refinancing might be an option to secure a lower interest rate or a different repayment term. However, refinancing federal loans into a private loan means losing access to federal benefits like IDR plans and forgiveness programs. This decision should not be taken lightly.

5. Stay Informed About Policy Changes

Student loan policies can change rapidly, often due to legislative action or Department of Education announcements. Regularly check official sources like StudentAid.gov, reputable financial news outlets, and government websites for updates relevant to student loan 2026. Subscribe to email alerts from your loan servicer and the Department of Education.

6. Re-certify Your Income Annually for IDR Plans

If you are on an IDR plan, you must re-certify your income and family size annually. Failing to do so can lead to your payments increasing significantly and capitalized interest. Mark your calendar and ensure you complete this process on time to maintain your eligibility and appropriate payment amount for student loan 2026.

7. If Eligible, Pursue Forgiveness Programs Diligently

For those pursuing PSLF or other forgiveness programs, meticulous record-keeping is essential. Track your payments, employment history, and submit any required forms (like the PSLF Employment Certification Form) regularly. Don’t wait until the last minute. Every step counts towards reaching your forgiveness goal. The requirements for these programs can be complex, and even minor errors can lead to delays or denials.

The Impact of Economic Factors on Student Loan 2026

Beyond specific policies, broader economic conditions will also influence the student loan 2026 environment. Factors such as inflation, interest rates, and the job market can affect borrowers’ ability to repay their loans and the overall cost of borrowing.

Interest Rates and Their Implications

Federal student loan interest rates are set annually by Congress and are fixed for the life of the loan. However, private loan interest rates can be variable or fixed, and they are influenced by market conditions. A rising interest rate environment could make private loans more expensive and potentially increase the cost of refinancing. Understanding the prevailing interest rate trends is crucial when making borrowing or refinancing decisions.

Inflation and Purchasing Power

High inflation can erode the purchasing power of your income, making it harder to afford monthly loan payments. While IDR plans adjust payments based on income, other plans do not. This makes the choice of repayment plan even more critical in an inflationary environment, as it directly impacts your disposable income and financial flexibility as you manage your student loan 2026 obligations.

Job Market Conditions

A strong job market with good wage growth can make it easier for borrowers to manage their student debt. Conversely, a weak job market or economic downturn can increase financial stress. The ability to find stable employment and earn a sufficient income is foundational to effective student loan repayment. As such, monitoring economic forecasts and career opportunities relevant to your field will be an indirect but important aspect of preparing for student loan 2026.

Common Pitfalls to Avoid in Student Loan Management

Even with comprehensive knowledge, borrowers can fall into common traps. Being aware of these can help you steer clear of unnecessary financial distress:

- Ignoring Your Loans: Burying your head in the sand is perhaps the worst strategy. Unpaid loans can lead to default, severely damaging your credit score and potentially leading to wage garnishment or tax refund offset. Proactive engagement with your loan servicer and understanding your options is always the best approach.

- Missing Re-certification Deadlines: For IDR plans, missing your annual re-certification can cause your payments to spike and unpaid interest to capitalize, increasing your principal balance.

- Not Understanding Forgiveness Requirements: Many borrowers assume they qualify for forgiveness programs without fully understanding the stringent requirements. Always verify your eligibility and track your progress carefully.

- Falling for Scams: Be wary of companies promising quick or easy loan forgiveness for a fee. The Department of Education and your loan servicer are the only legitimate sources for managing your federal student loans. Never pay for services you can get for free.

- Refinancing Federal Loans Without Understanding Consequences: As mentioned, refinancing federal loans into a private loan means forfeiting valuable federal protections. Ensure you fully grasp this trade-off before proceeding.

Future Outlook and Potential Legislative Changes for Student Loan 2026

The political landscape can significantly impact student loan policy. While predicting future legislative changes is challenging, it’s safe to assume that student loan debt will remain a topic of public discourse and potential reform. Any significant changes are likely to focus on:

- Further Enhancements to IDR Plans: The SAVE Plan is a testament to the ongoing effort to make repayment more manageable. It’s possible we could see further refinements or new IDR options introduced.

- Expansion of Forgiveness Programs: There’s continuous pressure to expand eligibility for existing forgiveness programs or introduce new ones, particularly for specific professions or low-income borrowers.

- Interest Rate Reforms: Discussions around lowering federal student loan interest rates or capping them are perennial. While immediate changes aren’t guaranteed, this remains a potential area for legislative action.

- Addressing the Cost of Higher Education: Ultimately, reducing the burden of student debt also involves addressing the rising cost of tuition. While not directly about loan repayment, policies aiming to curb college costs could indirectly impact future borrowing needs and the overall student loan 2026 outlook.

It is important for borrowers to remain adaptable and informed. What is true today regarding student loan policy might evolve by 2026, and staying connected to official government channels will be your best defense against misinformation and the best way to leverage new opportunities.

Conclusion: Empowering Your Student Loan Journey in 2026

The journey of student loan repayment can feel long and complex, but with the right information and proactive strategies, it is entirely manageable. As we look towards student loan 2026, the emphasis remains on understanding your specific loan types, exploring all available repayment and forgiveness options, and staying informed about policy changes. The new SAVE Plan, coupled with existing IDR and forgiveness programs, offers significant relief for many. However, these benefits are only accessible if you actively engage with your loan servicer and the Department of Education.

Take the time to review your financial situation, project your future income, and utilize the tools provided by StudentAid.gov. Don’t hesitate to contact your loan servicer for personalized advice, or seek guidance from a reputable, non-profit credit counselor if you feel overwhelmed. By taking these steps, you can confidently navigate the student loan 2026 landscape, minimize your financial burden, and pave the way for a more secure financial future.

Remember, you are not alone in this journey. Millions of borrowers are working through similar challenges, and the resources and programs available are designed to help. Empower yourself with knowledge, take decisive action, and set yourself on a path to successful student loan management.