Social Security 2026: COLA, Eligibility & Future Outlook

Social Security 2026: What Beneficiaries Need to Know About COLA and Eligibility

As we approach the mid-2020s, millions of Americans are keenly focused on the future of Social Security. Specifically, the year 2026 holds significant interest for current retirees, those nearing retirement, and financial planners alike. Understanding the potential changes, particularly regarding Cost-of-Living Adjustments (COLA) and eligibility criteria, is paramount for effective financial planning. This comprehensive article delves into the anticipated landscape of Social Security 2026, offering insights into what beneficiaries can expect and how these developments might impact their financial well-being.

The Cornerstone of Retirement: Understanding Social Security

Social Security has long served as a vital financial safety net for American workers and their families. Established in 1935, its primary goal is to provide a steady income stream for retirees, disabled individuals, and survivors of deceased workers. For many, Social Security benefits represent a significant portion, if not the entirety, of their retirement income. Therefore, any adjustments or shifts in the program, especially those concerning the annual Cost-of-Living Adjustment (COLA), can have profound effects on the purchasing power and financial stability of beneficiaries.

The program operates on a pay-as-you-go system, where current workers’ contributions fund the benefits of today’s retirees and other beneficiaries. This intergenerational contract underscores the importance of the program’s long-term solvency and adaptability to changing economic conditions. As demographics shift and economic pressures evolve, the need to regularly evaluate and adjust Social Security becomes increasingly critical. This is precisely why discussions around Social Security 2026 are so pertinent, as they touch upon the program’s ability to meet its commitments in the years to come.

Decoding COLA: The Heart of Annual Benefit Adjustments

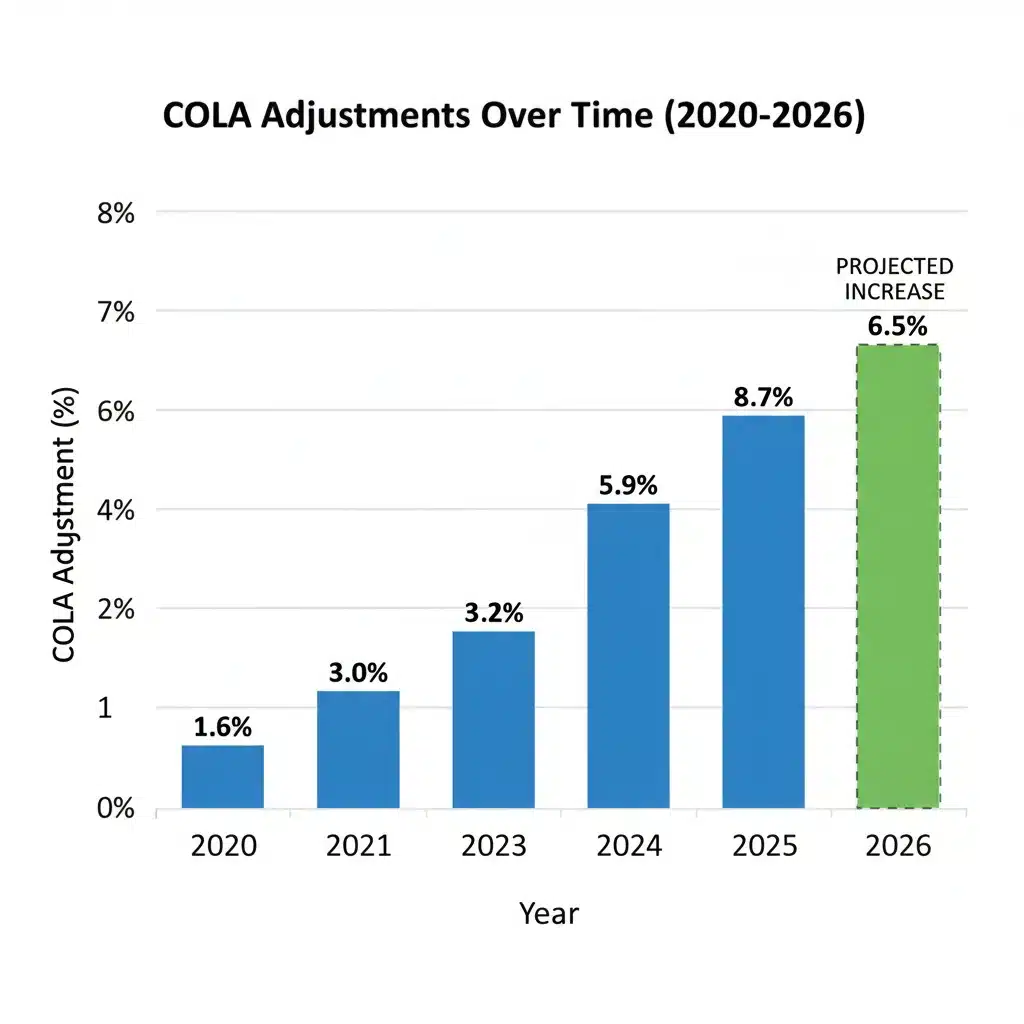

What is COLA?

The Cost-of-Living Adjustment, or COLA, is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its purpose is to help maintain the purchasing power of these benefits by offsetting the effects of inflation. Without COLA, the fixed income of retirees would gradually lose value over time, making it harder to afford essential goods and services.

The Social Security Administration (SSA) calculates COLA based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, it compares the average CPI-W for the third quarter of the current year (July, August, and September) with the average for the third quarter of the previous year. If there’s an increase, that percentage difference becomes the COLA for the following year. This calculation method is crucial to understanding potential future adjustments, including those for Social Security 2026.

Historical COLA Trends and Their Implications

Looking back at historical COLA trends provides valuable context. In some years, particularly during periods of low inflation, COLA has been minimal or even zero. Conversely, periods of high inflation, such as those experienced recently, have led to more substantial COLA increases. These fluctuations directly impact the monthly checks received by beneficiaries, highlighting the importance of accurate projections and robust financial planning.

For instance, a higher COLA might seem beneficial on the surface, but it often reflects a broader economic environment where everyday expenses are also rising rapidly. This means that while benefits increase, the cost of living may increase at a similar or even faster rate, potentially eroding the real value of the adjustment. Understanding this dynamic is key to assessing the true impact of COLA on personal finances, especially when considering the outlook for Social Security 2026.

Projecting COLA for Social Security 2026

Predicting the exact COLA for 2026 at this stage is challenging, as it depends heavily on economic conditions, particularly inflation rates, in the preceding years. However, various economic forecasts and expert analyses can provide a reasonable range of expectations. Factors influencing the 2026 COLA will include:

- Inflationary Pressures: The primary driver of COLA is inflation, as measured by the CPI-W. Ongoing global economic trends, supply chain issues, energy prices, and wage growth will all play a role in shaping inflation rates leading up to 2026.

- Federal Reserve Policies: The actions of the Federal Reserve in managing interest rates and the money supply can significantly impact inflation. Their decisions in the coming years will indirectly influence the COLA calculation.

- Geopolitical Events: Unforeseen global events, such as conflicts or pandemics, can disrupt economies and supply chains, leading to unexpected inflationary spikes or downturns.

While specific numbers remain speculative, financial analysts typically monitor economic indicators closely to offer projections. Beneficiaries should keep an eye on official announcements from the Social Security Administration, usually made in October of the preceding year, for the definitive COLA percentage. For Social Security 2026, this announcement would typically occur in October 2025.

Eligibility Requirements for Social Security 2026

Beyond COLA, understanding eligibility for Social Security benefits is fundamental. The requirements are generally stable but can be complex, involving work credits, age, and various life circumstances. For Social Security 2026, the core eligibility criteria are expected to remain consistent with current regulations, though it’s always wise to stay informed of any legislative changes.

Work Credits: The Foundation of Eligibility

To qualify for Social Security retirement benefits, individuals must earn a certain number of work credits. In 2024, you earn one work credit for each $1,730 of earnings, and you can earn a maximum of four credits per year. Most people need 40 credits, equivalent to 10 years of work, to be eligible for retirement benefits. These requirements are not anticipated to change for Social Security 2026.

It’s important to note that these credits don’t have to be earned consecutively. The SSA tracks your lifetime earnings, and as long as you accumulate the necessary 40 credits, you’ll be eligible. However, the amount of your benefit will depend on your average indexed monthly earnings (AIME) over your 35 highest-earning years.

Full Retirement Age (FRA)

Your Full Retirement Age (FRA) is the age at which you are entitled to receive 100% of your primary insurance amount (PIA). This age depends on your birth year:

- Born 1943-1954: FRA is 66

- Born 1955: FRA is 66 and 2 months

- Born 1956: FRA is 66 and 4 months

- Born 1957: FRA is 66 and 6 months

- Born 1958: FRA is 66 and 8 months

- Born 1959: FRA is 66 and 10 months

- Born 1960 or later: FRA is 67

For individuals planning to claim benefits in Social Security 2026, understanding their specific FRA is crucial. Claiming benefits before your FRA will result in a permanent reduction of your monthly payments, while delaying beyond your FRA (up to age 70) can lead to increased benefits through delayed retirement credits.

Early and Delayed Retirement Benefits

While FRA is the benchmark, you can choose to start receiving Social Security retirement benefits as early as age 62. However, doing so will result in a permanent reduction of your monthly benefit amount. The reduction percentage depends on how many months early you claim. Conversely, if you delay claiming benefits past your FRA, you can earn delayed retirement credits, which increase your monthly benefit for each month you delay, up to age 70.

For someone reaching their FRA in Social Security 2026, these choices can significantly impact their lifetime benefits. It’s a complex decision that should be made after careful consideration of personal health, financial needs, and other retirement income sources.

Maximum Taxable Earnings and Their Impact

Each year, the Social Security Administration announces a maximum amount of earnings subject to Social Security taxes. Earnings above this limit are not taxed for Social Security purposes, and they do not count towards your Social Security benefit calculation. This limit typically increases annually with average wage growth.

For Social Security 2026, this maximum taxable earnings limit is expected to be higher than in previous years, reflecting ongoing wage inflation. This adjustment primarily affects high-income earners, as it means a larger portion of their income will be subject to Social Security taxes. While it doesn’t directly impact the COLA, it’s an important aspect of the program’s funding and overall financial health.

Understanding Social Security’s Financial Outlook Towards 2026 and Beyond

The long-term solvency of Social Security is a perennial topic of discussion. Each year, the Social Security Board of Trustees releases a report detailing the financial status of the program and projecting its future. These reports often highlight the need for legislative action to ensure the program’s ability to pay 100% of promised benefits long-term.

For Social Security 2026, the program is expected to continue paying full benefits. However, the Trustees’ reports typically project that the trust funds could be depleted in the 2030s if no legislative changes are made. Should this occur, Social Security would still be able to pay a significant portion of benefits (around 80%) from ongoing tax revenues, but not the full scheduled amounts.

Potential solutions discussed to address long-term solvency include:

- Raising the Full Retirement Age: Gradually increasing the FRA further.

- Increasing the Payroll Tax Rate: Raising the percentage of earnings that workers and employers contribute.

- Adjusting the Maximum Taxable Earnings: Eliminating or raising the cap on earnings subject to Social Security taxes.

- Modifying the COLA Formula: Changing how the annual Cost-of-Living Adjustment is calculated.

- Means-Testing Benefits: Reducing benefits for high-income retirees.

While these are policy debates that may or may not translate into legislation by Social Security 2026, beneficiaries and taxpayers should be aware of the ongoing discussions and their potential implications for the program’s future. The stability of Social Security is a critical component of national economic security.

Planning for Your Retirement with Social Security 2026 in Mind

Given the potential for COLA adjustments and the ongoing discussions about the program’s long-term financial health, proactive retirement planning is more important than ever. Relying solely on Social Security benefits is often insufficient for maintaining a comfortable lifestyle in retirement. Here are some strategies to consider:

Diversify Your Retirement Savings

Supplementing Social Security with other retirement savings vehicles is crucial. This includes 401(k)s, IRAs (Traditional or Roth), and personal savings accounts. A diversified portfolio can help mitigate risks and provide a more robust financial foundation for your golden years. The more you save independently, the less vulnerable you will be to any potential changes in Social Security 2026 or beyond.

Understand Your Benefit Statement

Regularly review your Social Security statement, which you can access online through your My Social Security account. This statement provides a personalized estimate of your future benefits based on your earnings record. It’s an invaluable tool for planning and identifying any discrepancies in your reported earnings. Knowing your estimated benefit can help you project your income for Social Security 2026 and subsequent years.

Consider Working Longer

If feasible, working a few extra years can significantly boost your Social Security benefits in two ways: it allows you to earn more work credits (if needed) and, more importantly, it increases your average indexed monthly earnings (AIME), which is used to calculate your benefit amount. Additionally, delaying your claim past your FRA can earn you delayed retirement credits, as discussed earlier. This strategy can be particularly impactful for those nearing retirement in the years leading up to Social Security 2026.

Seek Professional Financial Advice

A qualified financial advisor can help you integrate your Social Security benefits into a comprehensive retirement plan. They can assist with strategies for claiming benefits, managing investments, and ensuring you are prepared for potential economic shifts, including those that might influence Social Security 2026.

The Application Process for Social Security Benefits

When the time comes to apply for Social Security benefits, the process is relatively straightforward. You can apply online, by phone, or in person at a local Social Security office. Most people find the online application to be the most convenient method.

It’s generally recommended to apply for benefits about three months before you want your benefits to start. This gives the SSA ample time to process your application and avoids any delays in receiving your first payment. Ensure you have all necessary documentation, such as your birth certificate, W-2 forms or self-employment tax returns, and bank account information for direct deposit.

For those aiming to start benefits in Social Security 2026, planning ahead and understanding the application timeline will be crucial for a smooth transition into retirement.

Staying Informed: Your Role as a Beneficiary

The landscape of Social Security is dynamic, influenced by economic factors, legislative decisions, and demographic shifts. As a current or future beneficiary, staying informed is your best defense against uncertainty. Regularly checking official SSA resources, reputable financial news, and expert analyses can help you anticipate changes and adjust your financial plans accordingly.

The discussions surrounding Social Security 2026 are part of a continuous national dialogue about securing the financial future of millions. By understanding how COLA is calculated, what eligibility entails, and the broader financial health of the program, you empower yourself to make informed decisions and advocate for policies that support a strong and sustainable Social Security system for generations to come. Your active engagement and informed perspective are vital in ensuring this cornerstone of American retirement continues to serve its purpose effectively.

Conclusion: Preparing for Social Security 2026 and Beyond

The prospect of Social Security 2026 brings with it a mix of anticipation and the need for prudent financial planning. While the exact COLA percentage will not be known until late 2025, understanding the mechanisms behind these adjustments and the underlying eligibility requirements is essential. The program’s long-term financial outlook, though subject to ongoing debate and potential legislative action, highlights the importance of diversified retirement savings and proactive engagement.

For current and future beneficiaries, the message is clear: Social Security is a foundational element of retirement security, but it should ideally be part of a broader financial strategy. By staying informed about COLA projections, understanding your eligibility, and actively planning for your financial future, you can navigate the changes of Social Security 2026 and beyond with confidence, ensuring a more secure and comfortable retirement.

Contributions to $23,000")